In the previous blog post, the topic of the economic recovery was discussed. Although it has been a solid recovery, why doesn’t it feel more robust?

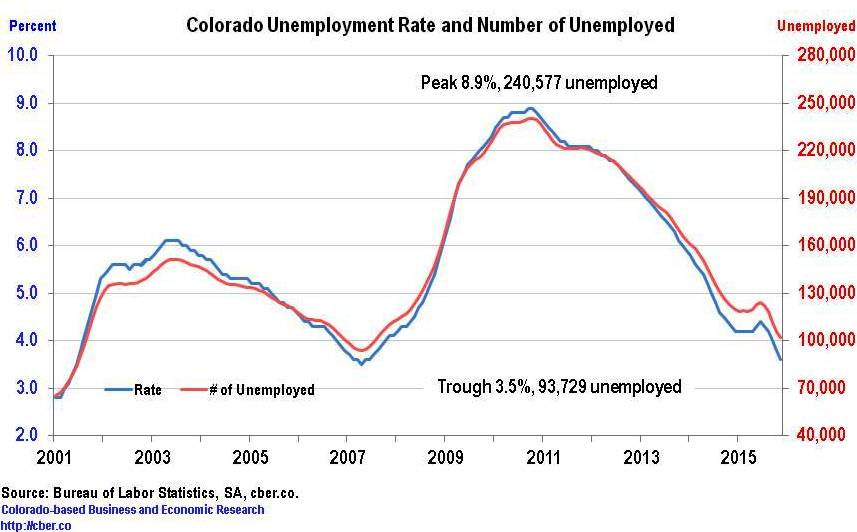

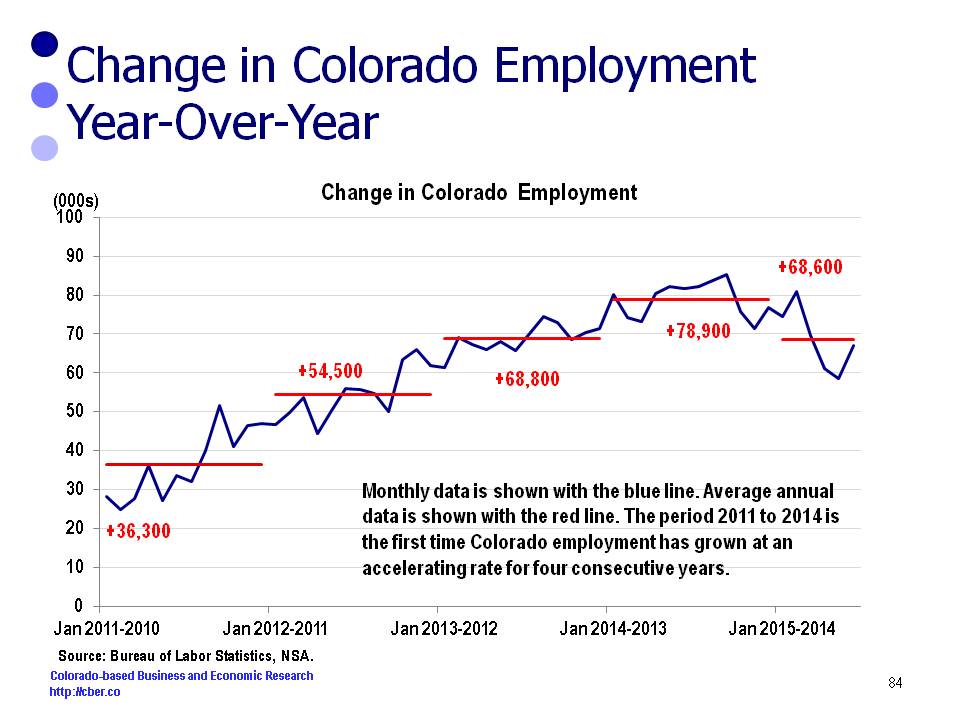

The 2007 recovery was atypical in that it occurred over a period of years, as opposed to months. As a result Colorado posted accelerating job growth for four consecutive years. Essentially, the recovery from the recession was weak and gradual. At no point has the state reached a point where public and private leaders could really say, “We have arrived.”

At the national level, the U.S. will add 3.0 million jobs in 2015. Yet, the focus is on the slowdown of the global economy, not the fact that 2015 will be the fifth consecutive year of solid job growth.

Nationally, GDP growth has been subpar. It is hard to get excited when the rate of Real GDP growth is 2.0% to 2.5%. Consumer spending has increased at a similar anemic rate. In other words consumers have remained cautious, as if they are always looking over their shoulder.

The construction industry is “booming” and there is a shortage of trained workers. At the same time, the growth of the industry pales when compared to the 2000s. The good news is that housing has been built on an “as needed basis” and the chance of being overbuilt is slim.

During the recovery period, the state has suffered natural tragedies. There were multiple severe forest fires in several parts of the state, as well as flooding and drought. That was taxing on the state – fiscally and psychologically. Fortunately, Coloradans have remained resilient.

Lower oil prices have dampened growth in parts of the state that had previously experienced strong growth. It is easy to forget the risk associated with the extractive industries until the price of the commodities (oil, molybdenum, coal) drops precipitously or regulations are established that eliminate demand for these commodities.

Then there is the state government… The legislature has focused on social issues for the past couple of sessions – and that is not bad. Some feel insufficient time and resources were spent addressing issues that could improve the state’s ability to conduct business.

At one point, there was sufficient discourse to cause several counties to threaten secession from the state. At times, state government seemed dysfunctional over the past five years.

State government faces a new problem – the state economy is on solid footing and the state will generate record levels of revenue, yet the legislature will be forced to make cuts to key service areas. This conundrum is caused by the combination of Amendment 23, the Gallagher Amendment, TABOR, the initiative process, and Medicare obligations. It is difficult for legislators to govern the state in a way they feel is appropriate.

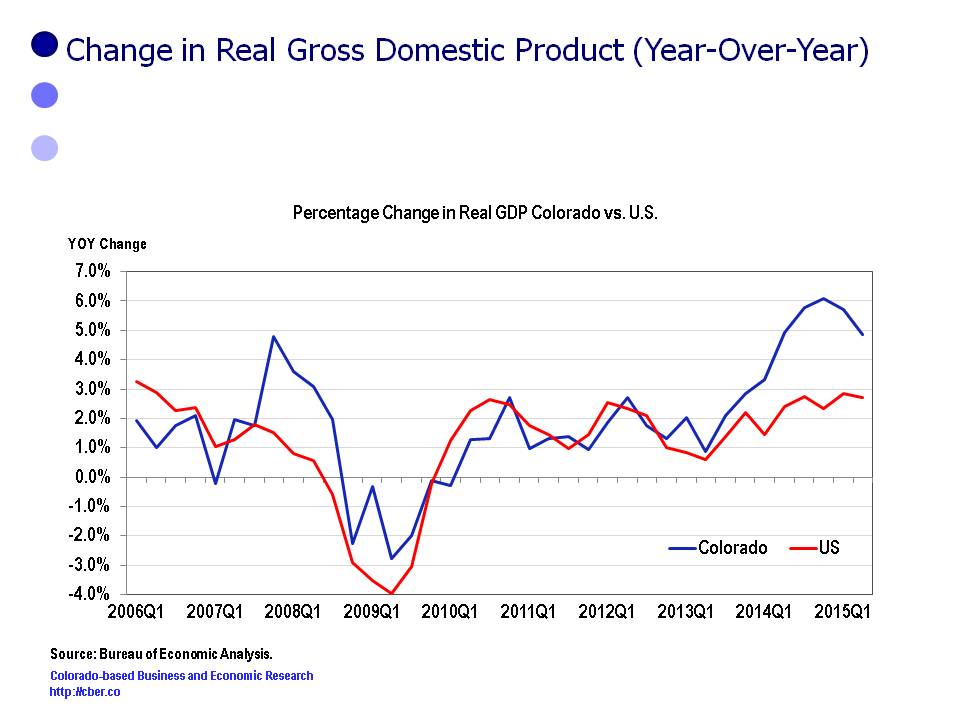

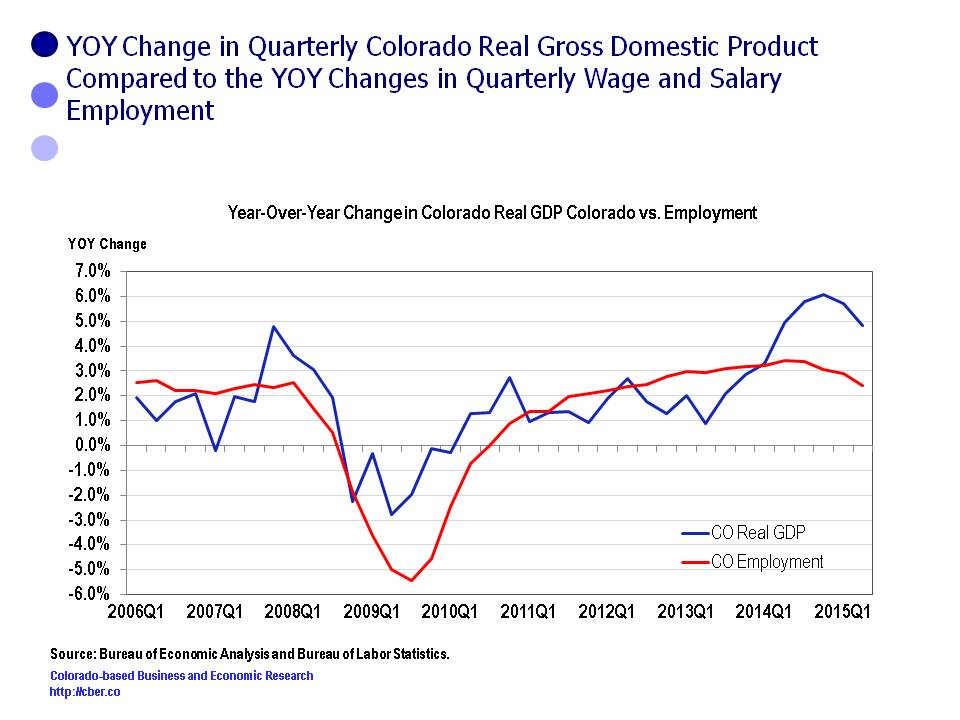

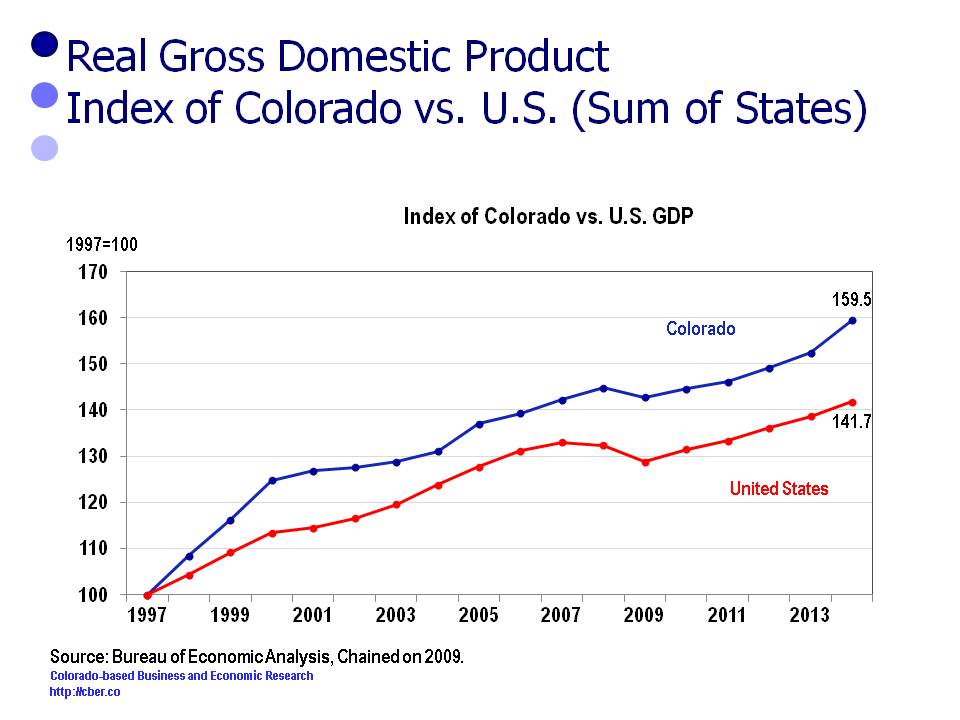

Despite the challenges and angst created by the items mentioned above, the growth of Colorado’s economy has exceeded the growth of the U.S. economy in many key areas (rate of job growth, rate of population growth, growth of Gross Domestic Product).

Unfortunately, the picture hasn’t always been rosy for the past five years, despite the many great things that have happened.