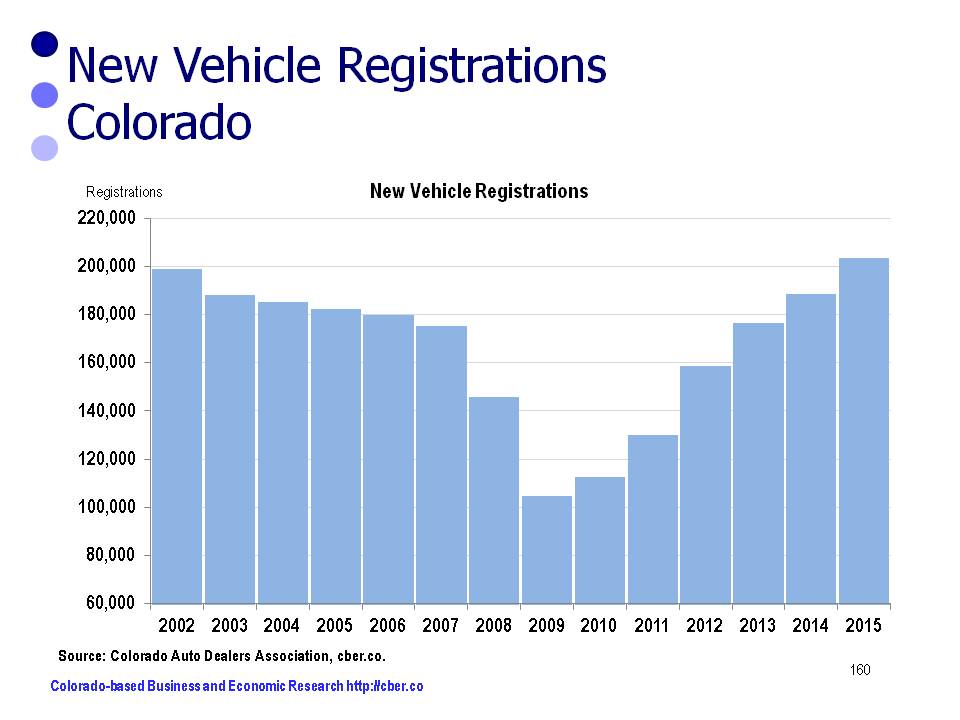

Recently, a local economist hypothesized that the recent strength of the Colorado economy was correlated with a warmer winter. The rationale for this hypothesis was that warmer weather may have benefitted outdoor sports such as golf courses, biking, rollerblading, and so forth. In addition, the economist surmised that retail sales would be stronger because warmer weather was more conducive to shopping and increased construction activity.

On one hand, the warmer weather theory sounded plausible because the weather “seemed” milder this winter, but on the other hand it sounded like it was full of hot air.

Premise 1 – The winter was warmer.

If heating degree days are the defining factor for how cold a winter is, then the period October 2011 through March 2012 was negligibly colder than the prior year. For this six month period, the most recent October, December, and February were colder, the two Novembers were similar, and January and March were warmer this year. (A larger number means it is colder, more heat is needed to heat a building).

October 2010 174 heating degree days

November 2010 645 heating degree days

December 2010 789 heating degree days

January 2011 925 heating degree days

February 2011 863 heating degree days

March 2011 513 heating degree days

Total 3,909 heating degree days

October 2011 312 heating degree days

November 2011 636 heating degree days

December 2011 1,058 heating degree days

January 2012 763 heating degree days

February 2012 935 heating degree days

March 2012 364 heating degree days

Total 4,068 heating degree days

Possibly it seemed warmer, because there didn’t seem to be snow on the ground that often. A comparison of snowfall for the metro area shows that there was 2.5 times as much snow this past winter as the prior year.

October 2010 none

November 2010 1.5 inches

December 2010 3.3 inches

January 2011 8.0 inches

February 2011 5.3 inches

March 2011 2.5 inches

Total 20.6 inches

October 2011 8.5 inches

November 2011 4.5 inches

December 2011 16.5 inches

January 2012 4.9 inches

February 2012 20.2 inches

March 2012 none

Total 54.6 inches

It is truly a shocker to learn that the past winter was actually colder and wetter than the previous year. The timing of the storms, the lack of wind, or some other factor must have created the perception that it was warmer this past winter.

Even with greater snowfall in the metro area, snowpack is below average and 95% of Colorado is reportedly in drought conditions. Two significant forest fires have occurred and summer hasn’t arrived.

Conclusion: Premise 1 is FALSE.

Premise 2 – The warm weather resulted in increased participation for local sporting activities.

There is no easy way to prove this. HOWEVER, the lack of snow in the ski country, at the right times, was in part responsible for diminished lift ticket sales – a decrease of more than 7%. Ouch that hurts! Not only did the lack of snow hurt ski business it will play havoc with rafting businesses this summer.

Conclusion: #2 Possibly true in the metro areas, FALSE in ski areas.

Premise 3 – Warm weather means stronger retail sales.

This is an interesting concept that is difficult to prove. Cold and snowy weather on key shopping days have reduced retail sales during past Christmas shopping seasons, but there is no evidence that warmer weather has increased trade sales. Retail sales are noticeably higher compared to a year ago, but that is attributed to more people working than last year at this time. And in some cases, sales are higher because retailers have finally been able to raise prices. Sales may be higher in the metro areas, but they are probably below expectations in the ski country because of reduced traffic.

Conclusion: #3 – Possibly true in the metro area, FALSE in ski areas.

Premise 4 – Warm weather means increased construction activity.

For the six month period October to March there were 114,500 construction workers this year versus 113,300 last year. Last June, the Construction sector finally bottomed out from the 2007 recession and has been slowly adding jobs since. The big boost of construction jobs in January is more likely a result of improved economic conditions than warmer weather.

Conclusion:#4 – Inconclusive.

One of the fun things about economics is dissecting “grassy knoll” or “warmer weather” theories to see if they are true, partially true, or false. In this case, it is highly improbable that the “warmer” weather was a source of net job creation. The gains in revenue at Denver golf courses, bike shops, and shopping malls were offset by losses on the ski slopes and sales in mountain t-shirt shops, hotels, and restaurants. The warmer weather will also result in a dismal rafting season and increased costs for fighting forest fires.

For a more complete update on the recovery of the Colorado economy, go to https://cber.co/.

©Copyright 2011 by CBER.