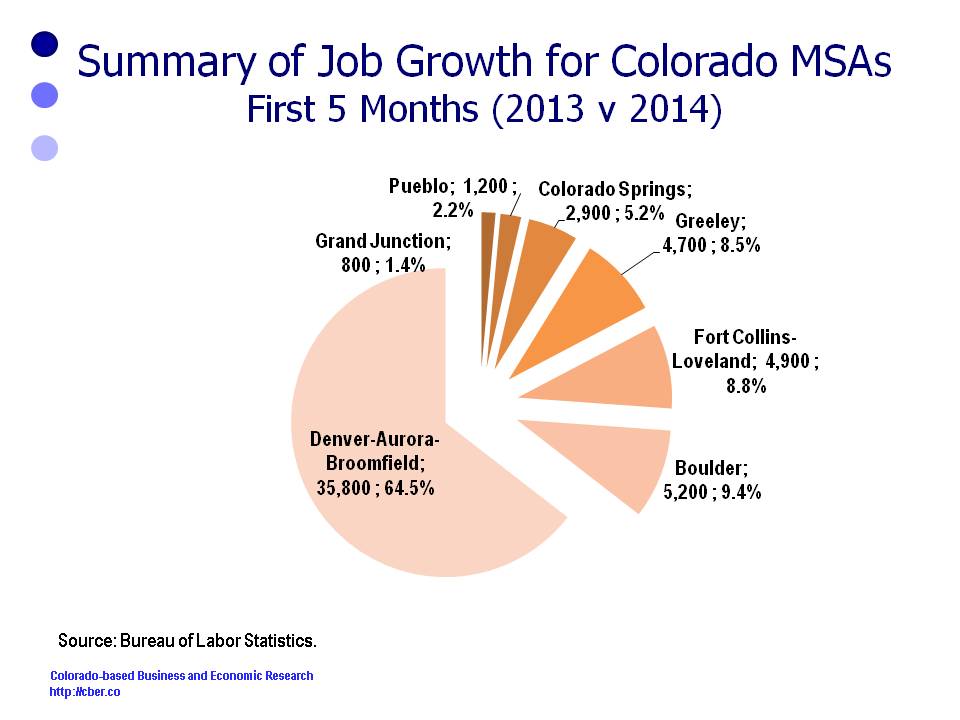

Is Colorado adding too many low-wage jobs?

When analyzing the job changes in an economy there are several points that are understood. For example:

- Jobs are often added unevenly. For instance, during expansionary periods construction jobs will usually be added at a faster pace than other jobs.

- All jobs are important to the economy for different reasons. Some jobs provide basic services while others generate tax revenue.

- Some jobs have higher than average wages while others have lower than average wages. There is often greater consumption when workers are paid higher wages.

For the past seven months the following five sectors account for about 45% of total jobs in the state, yet they are responsible for almost 75% of the jobs added this year.

- Accommodations and Food Services

- Health Care

- Construction

- Professional and Scientific Services

- Retail Trade.

The following information includes the top sectors, the average annual private sector wages for the sectors, and the reasons those sectors are important. The average private sector wages $50,768.

- Accommodations and Food Services, $18,808. About 10% of all jobs are in the Accommodations and Food Services sector. AFS has accounted for about 20% of the jobs added this year. As a major component of the tourism sector, AFS is an important part of the economy in all 64 counties.

- Health Care, $45,905. Just under 11% of the state’s s jobs are in the Health Care sector. This category has accounted for about 15% of total jobs added this year. The Health Care sector affects our quality of life and plays a key role in the economy in all 64 counties.

- Construction, $51,064. The Construction industry is small by comparison, with about 5.0% of total state jobs. Approximately 12% of the job growth is in this category. A segment of the Construction jobs are tied to the growth of the extractive industries.

- Professional, Scientific, and Technical Services, 84,842. A portion of the Professional, Scientific, and Technical jobs are a key part of the state’s advance technology industries. They account for about 8% of the jobs and 11% of the job growth.

- Retail Trade, $28,159. Retail Trade jobs account for almost 11% of total jobs and 11% of total job growth. The retail sector is critical to most local governments because a majority of their revenue is derived from retail trade sales taxes.

There is legitimate reason to be concerned that the state is adding so many low-wage jobs. On the other hand, it is a positive sign that the state is adding jobs that potentially impact all counties, jobs are being added in sectors that generate tax revenues, and jobs are being added that allow for a better quality of life.

So, is Colorado adding too many low-wage jobs?