Looking ahead to 2015 there are three issues that will impact the economy in 2015: healthcare, extractive industries, and wages.

Healthcare

The healthcare industry may play an important role in the economy in 2015.

• First, there are shortages of workers in many key positions. This may affect the care consumers receive from their service providers and it may increase the costs of doing business.

• Second, providers are being pushed by Obamacare and insurance companies to reduce the fees they charge. In turn, this may reduce their margins.

• Third, it was recently announced that Colorado employers will face an 8% increase in the cost of insurance. Likely, a portion of that increase will be passed on to workers. That could reduce that amount of discretionary income, which in turn could reduce retail consumption.

• In addition, it has been announced that Connect for Health Colorado, will reduce subsidies. In other words, many Coloradans will have to pay significantly more for coverage, go without healthcare, or pay a fine to the government. Coloradans will face sticker shock when they get their health insurance bills in 2015.

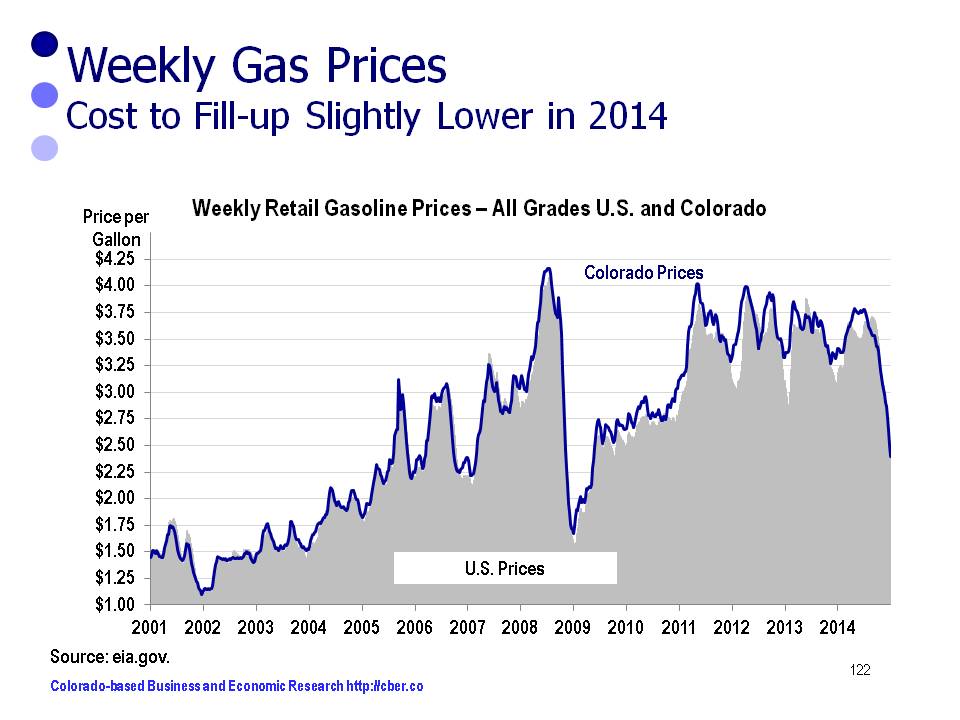

Extractive Industries and Prices of Oil and Gasoline

The extractive industries will continue to face challenges in 2015. Fracking is still an issue in Colorado that will not go away. Local governments are pushing to have greater control over the way the extractive industries operate in their jurisdiction.

In addition, the price of oil has trended downward for the past six months. If these trends continue, it may impact production in Colorado, which will hit the smaller companies first. It will also impact severance taxes paid to the state government.

At the same time consumers have enjoyed lower prices at the pump. Their gasoline bills for 2013 and 2014 will be similar. If lower prices continue into 2015, consumers may notice a reduction in their annual gasoline bill in the range of $400 to $800 for the year.

If prices at the pump continue to decline Colorado consumers will be the benefactors, but state coffers suffer. Typically the negative impact for the state outweighs the positive impact on the consumer.

Wages

Typically, when unemployment dips below the natural rate of employment, 4.5% to 5.0%, there is usually upward pressure on wages. Overall that has not been the case in Colorado.

Between 2007 and 2014

• The Denver Boulder Greeley CPI (DBG) increased at an annualized rate of 2.4%

• The Private Sector Average Weekly Wages (AWW) increased by an annualized rate of 1.7%.

Inflation for this period grew at a faster rate than private wages for this period.

Between 2013 and 2014

• The DBG CPI is projected to increase by 2.8%/

• The Private Sector AWW will increase by 2.0%.

The Construction and Financial Activities are isolated sectors that have seen strong wage growth in the last couple of years because the demand for qualified employees has exceeded the supply of workers.

Construction Wages

• Between 2008 and 2012 AWW declined. In 2013 it increased by 11.0% followed by an increase of 11% in 2014. Construction businesses have found that it has been necessary to raise wages this amount to attract workers. Ultimately these labor costs will be passed on to consumers.

Financial Activities

• The financial activities sector has also had strong wage growth, 5.0% annualized growth, from 2007 to 2014. Between 2007 and 2010 Average Weekly Wages decreased, but they have increased significantly since. AWW will increase by 7.3% in 2014

On the other hand, 2014 inflation growth will exceed the change in wages for Manufacturing, Tourism, and Professional and Business Services. These three industries are critical to the state economy for different reasons.

Watch for healthcare, extractive industries, and wages to impact the Colorado Economy in 2015 – and the impact may not always be positive.